April 2, 2026

The surface story this week is a market grinding sideways. The S&P 500 is down roughly 4% on the month, the Nasdaq has shed nearly as much, and volatility has returned with a vengeance. But beneath that familiar headline, something more consequential is playing out — a meaningful reordering of where investors are placing near-term conviction. ETF flow data tells that story far more clearly than prices alone.

The message is hard to miss: capital is rotating out of the ideas that drove 2024 and into the physical realities of 2026.

Gold’s Paradox: Prices Up, Investors Out

Gold is the most important contradiction in this week’s data. GLD has gained nearly 23% over six months and is up more than 10% on the quarter. By every traditional measure, it is working exactly as a safe-haven should.

And yet investors are pulling money out at a striking pace. GLD has shed approximately $7.9 billion in the past month alone and over $2.9 billion year-to-date. Silver tells the same story — SLV is up nearly 59% over six months but has seen $1.9 billion leave in a single month.

This isn’t capitulation — it’s profit-taking at scale, most likely institutional investors using precious metals gains to cover losses elsewhere: in tech, in growth, in crypto. The metal is rising not because new money is arriving, but because commodity sellers haven’t materialized yet. That distinction matters for the weeks ahead. The macro drivers — dollar pressure, fiscal deficits, geopolitical friction — haven’t gone away. When the forced selling subsides, inflows could return quickly.

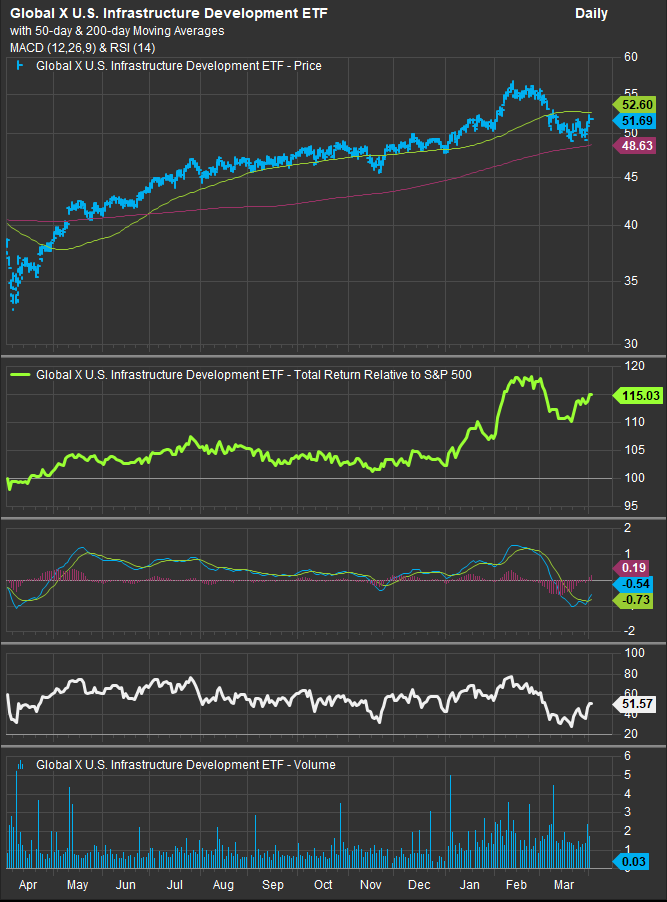

Defense and Infrastructure: Flows With Conviction

If there is one theme where price performance and fund flows are aligned heading into Q2, it is defense and infrastructure. ITA has attracted over $4 billion in one-year flows, with the geopolitical backdrop and domestic industrial spending agenda providing durable tailwinds. PPA has added $1.3 billion over the same period.

Infrastructure is equally compelling near-term. PAVE has pulled in over $1 billion year-to-date and $1.4 billion over twelve months, while IGF has attracted $2.4 billion in a year. These aren’t short-term trading flows — they represent allocations to a view that government-led capital expenditure is a reliable theme through the rest of 2026 regardless of the macro backdrop.

The three-month return profile confirms the trade is working: PAVE up over 8%, ITA up more than 4%, both outperforming the S&P 500 by a wide margin. This is a rotation with fundamental support behind it.

The Tariff Shock and the Oil Paradox

Energy is where the data gets interesting. XOP has surged 39% over three months and 14% in the past month. USO is up over 51% in a single month and 79% on the quarter — among the best-performing ETFs in the entire dataset right now.

But flows into the broader energy complex are decelerating, and some segments are seeing outflows despite the price action. The market appears to be treating this surge with skepticism — a tariff-driven dislocation rather than a demand-led rally. When prices move faster than fundamentals, sophisticated money tends to use the spike to reduce exposure rather than chase it.

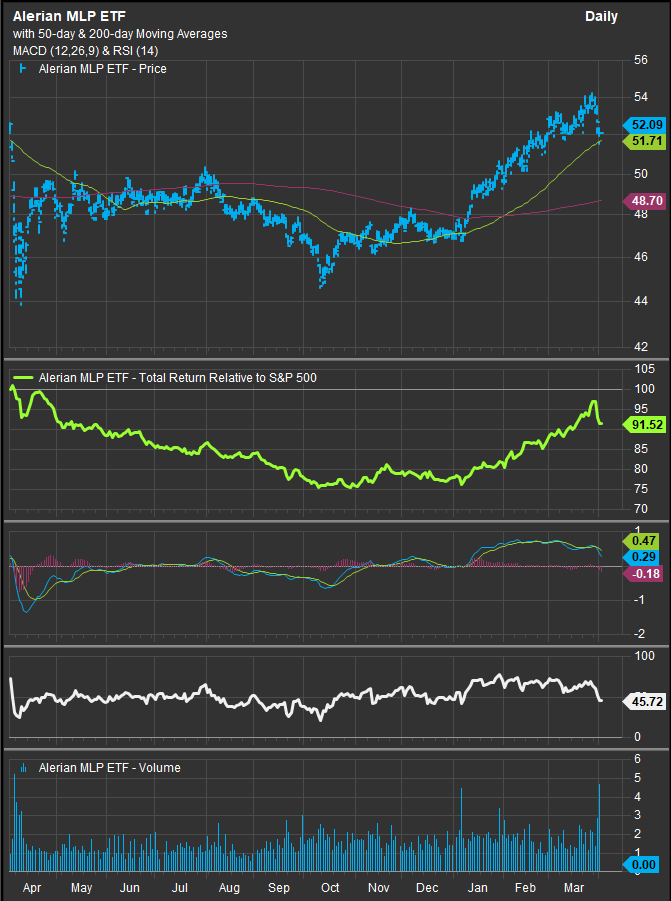

MLPs reinforce this read. Midstream vehicles like AMLP and EMLP are broadly flat to modestly positive on flows despite healthy 3-month returns in the 13–21% range. Investors like the income, but aren’t adding aggressively at these levels.

The short-term is anyone’s guess with headlines capturing the tape and equities under pressure at the market level. The main takeaway here is that investors are still treating legacy energy exposure as a trade rather than a durable buy-and-hold theme. Worth watching closely over the next few weeks for any shift in that posture.

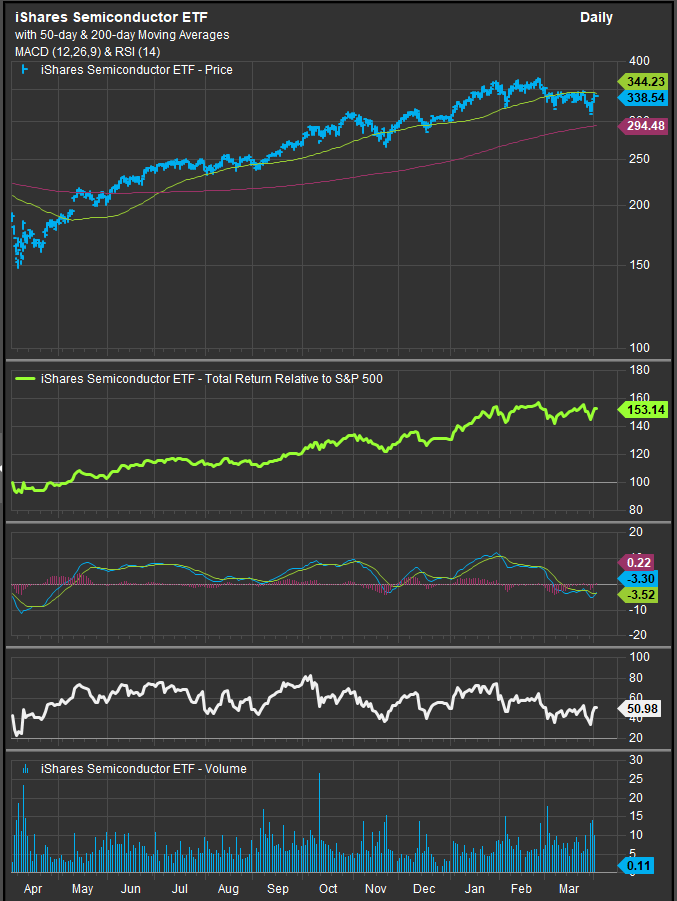

Semiconductors: The Durable AI Bet Holds

While the broader tech complex has struggled — QQQ down nearly 5% on the quarter and shedding flows — semiconductors have quietly become the most defensible part of the technology trade this quarter. SMH has attracted over $2 billion YTD and $6 billion over the past year. SOXX has added $1.1 billion this year. Both are positive on the quarter, bucking the tech selloff.

The divergence from software is sharp and telling. IGV is down nearly 25% on the quarter with RSI deep in oversold territory at 35. Cloud, internet, and SaaS-oriented products are all bleeding assets. Investors are making a deliberate near-term distinction: the physical infrastructure of AI — chips and the supply chain around them — holds its value in a risk-off environment, while the software layer is being repriced for slower growth and tighter conditions.

Blockchain’s Brutal Q1

The crypto and blockchain ETF universe had a rough first quarter and shows no sign of stabilizing. BKCH is down 35% over six months. CRPT has lost 48%. DAPP is off 33%. RSIs across the category sit in the low 40s, outflows are consistent, and there is no positive flow signal to suggest a near-term floor is forming.

The institutional adoption narrative that powered the category through late 2024 has stalled. What remains is a segment under pressure, with the risk-off environment stripping away the speculative premium that had built up across digital asset equities. Until risk appetite broadly improves, this category looks like a source of funds rather than a destination for them.

ESG: Quiet Pressure, Not Collapse

ESG ETFs aren’t collapsing, but the flow data shows quiet and persistent pressure. The largest funds — ESGU, ESGV — still hold substantial AUM, but most climate-focused and carbon-transition funds are in outflow. RSI readings across the complex cluster in the low-to-mid 40s.

KRBN (KraneShares Global Carbon Strategy) is a notable short-term exception — up nearly 3% on the month with an RSI of 73 — but at $131 million in AUM it remains a niche signal. The broader headwind through the rest of 2026: reduced institutional ESG mandates and continued underperformance relative to value and commodity-heavy alternatives that are dominating this year’s return tables.

The Factor Signal: Income Is Working, Growth Isn’t

One factor read stands out cleanly in this week’s data: income and value are outperforming growth, and flows are confirming it in real time. SCHD has attracted nearly $5 billion year-to-date and almost $7 billion over twelve months. VYM and DGRO are similarly drawing consistent inflows. Meanwhile VUG is down nearly 9% on the quarter and shedding assets.

Momentum is also holding better than expected — SPMO has added $6.1 billion over the past year — but what momentum is now tracking looks very different from 2024: energy, defense, miners, and infrastructure rather than mega-cap tech.

This Week’s Bottom Line

The ETF flow picture for the first week of April tells a coherent story: the near-term trade is rotating toward physical assets, sovereign spending themes, and income — and away from growth, software, crypto, and speculative tech. Gold is rising but profit-taking limits upside in the near term. Defense and infrastructure have the cleanest flow conviction. Energy’s surge is perceived as Geopolitical/tariff-driven rather than a structural shift. Semiconductors are holding while software breaks down.

Watch for gold inflows to resume as profit-taking exhausts itself. Watch for energy flows to either confirm or deny the commodity price spike over the next two to three weeks. And watch whether the infrastructure and defense bid holds if broader risk appetite improves — or deepens if it doesn’t.

Performance and flow data sourced from FactSet Research Systems Inc. as of April 2, 2026. This column is for informational purposes only and does not constitute investment advice.