COMMENTARY:

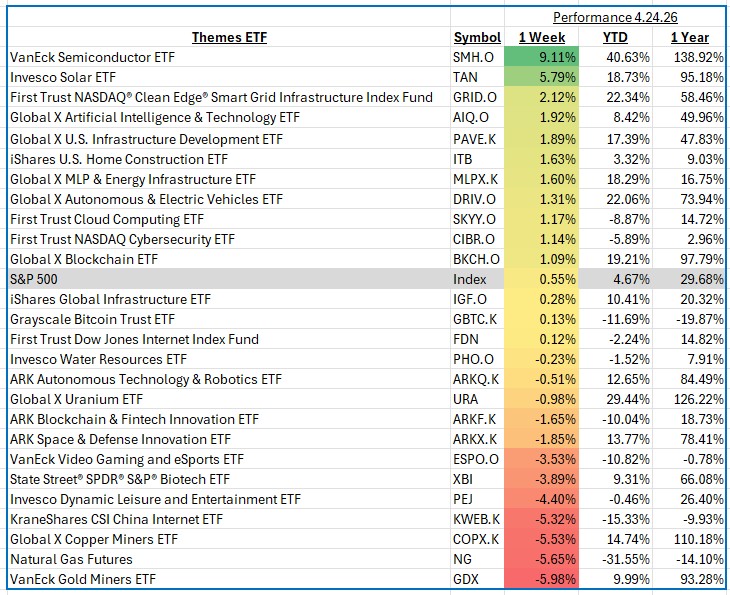

The S&P 500 was essentially flat for the week ending April 24, 2026, rising just 0.55% as investors navigated a mixed macro backdrop. Within thematic equities, performance dispersion remained pronounced. Key highlights included continued momentum in artificial intelligence–linked infrastructure, renewed interest in clean energy tied to policy support and falling input costs, and weakness in defensive and commodity-linked themes as growth expectations stabilized and real yields edged higher.

Across thematic exposures, leadership was concentrated in innovation-driven areas such as semiconductors, cloud computing, and digital infrastructure, alongside selective strength in renewable energy. Meanwhile, commodity-sensitive themes—including precious metals and natural gas—faced pressure from shifting rate expectations and softer underlying pricing trends. This divergence underscores how thematic investing continues to be driven by both structural growth narratives and short-term macro catalysts.

Innovation & Artificial Intelligence: Semiconductor exposure surged 9.1%, leading all themes for the week. Strength was driven by continued enthusiasm around AI infrastructure buildout, with standout contributions from NVIDIA, Taiwan Semiconductor Manufacturing Company, and ASML Holding. Investor optimism was reinforced by strong earnings commentary pointing to sustained demand for advanced chips and manufacturing capacity, while easing supply chain constraints further supported sentiment.

Clean Energy & Electrification: Solar-related exposure advanced 5.8%, benefiting from declining input costs, supportive policy frameworks, and improved financing conditions. Leaders included First Solar, Enphase Energy, and SolarEdge Technologies. Investors responded positively to improving margin outlooks and stabilization in installation demand, particularly in key U.S. and European markets.

Real Assets & Precious Metals: Gold miner exposure declined 6.0%, pressured by a pullback in gold prices as real yields moved higher and the U.S. dollar strengthened. Major detractors included Newmont Corporation, Barrick Gold, and Agnico Eagle Mines. The group’s sensitivity to macro variables—particularly interest rates—remained a key headwind during the week.

Energy Transition & Commodities: Natural gas-linked exposure fell 5.7%, reflecting weaker commodity pricing and concerns around oversupply. Companies such as EQT Corporation and Cheniere Energy were among the primary laggards, as mild weather trends and storage dynamics weighed on near-term demand expectations.

Overall, the week highlighted a continued rotation toward growth-oriented and innovation-led themes, while rate-sensitive and commodity exposures lagged. Markets remain highly responsive to both macro signals and earnings-driven narratives as investors position for the evolving economic landscape.