COMMENTARY:

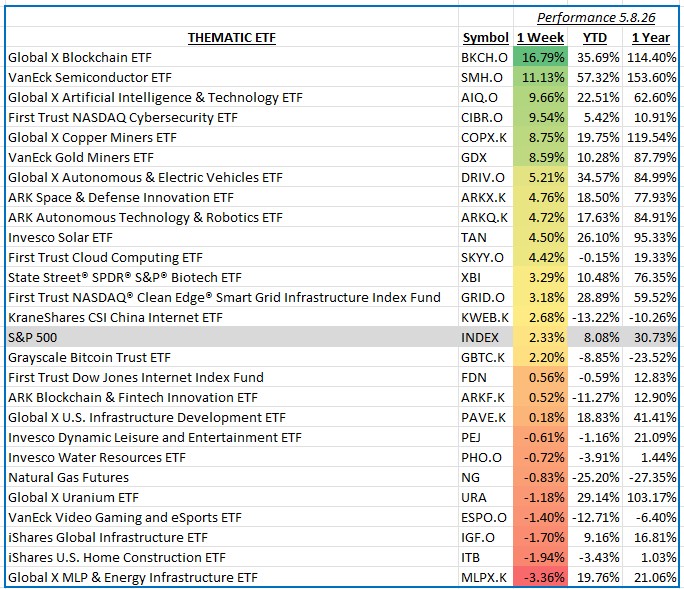

The S&P 500 advanced 2.33% for the week ending May 8, 2026, as investors continued rotating into higher-growth and innovation-oriented areas of the market. Within the thematic equity space, optimism surrounding artificial intelligence, digital infrastructure, and improving capital markets sentiment helped drive strong performance across several disruptive growth themes. Investor confidence was also supported by moderating inflation expectations, stable Treasury yields, and renewed enthusiasm for technology-driven earnings growth. Meanwhile, more economically sensitive and income-oriented themes lagged as commodity price weakness and concerns about slowing housing activity weighed on performance.

Blockchain-related equities delivered the strongest performance of the week, surging 16.8% as digital asset prices rallied sharply and investor appetite for speculative growth themes improved. Strength across the cryptocurrency ecosystem followed renewed institutional interest in digital assets and improving sentiment toward blockchain adoption and trading activity. Leading contributors included Coinbase, Marathon Digital Holdings, Riot Platforms, and CleanSpark, all of which benefited from higher cryptocurrency prices and stronger expectations for transaction volumes, mining profitability, and retail participation across digital markets.

Semiconductor companies also posted impressive gains, climbing 11.1% as investors continued to favor companies tied to artificial intelligence infrastructure, cloud computing, and advanced chip manufacturing. Positive earnings guidance, expanding data center demand, and expectations for sustained AI-related capital spending supported broad gains across the industry. Performance was led by mega-cap semiconductor and equipment manufacturers including NVIDIA, Taiwan Semiconductor Manufacturing Company, Broadcom, and Advanced Micro Devices. Investor enthusiasm remained concentrated in companies viewed as critical enablers of next-generation computing and enterprise AI deployment.

Energy infrastructure was among the weakest-performing thematic exposures, declining 3.4% as falling oil and natural gas prices pressured pipeline operators and midstream energy companies. Concerns about slowing global energy demand growth and weaker commodity pricing reduced investor appetite for income-oriented energy assets during the week. Large contributors to the downside included Enterprise Products Partners, Energy Transfer, and Kinder Morgan, which faced pressure alongside broader weakness across the energy complex.

Home construction-related equities also lagged, falling 1.9% as investors reacted to persistently elevated mortgage rates and signs of slowing housing affordability. Homebuilders and building product companies faced pressure as markets weighed the potential impact of higher financing costs on future demand. Weakness was most notable in D.R. Horton, Lennar, and PulteGroup, as investor sentiment toward the housing market softened modestly during the week.

Overall, thematic markets reflected continued investor preference for innovation-driven growth opportunities tied to artificial intelligence, semiconductors, and digital assets, while more cyclical and rate-sensitive themes faced renewed headwinds. Market leadership remained concentrated in areas benefiting from long-term technological transformation and improving risk appetite.