COMMENTARY:

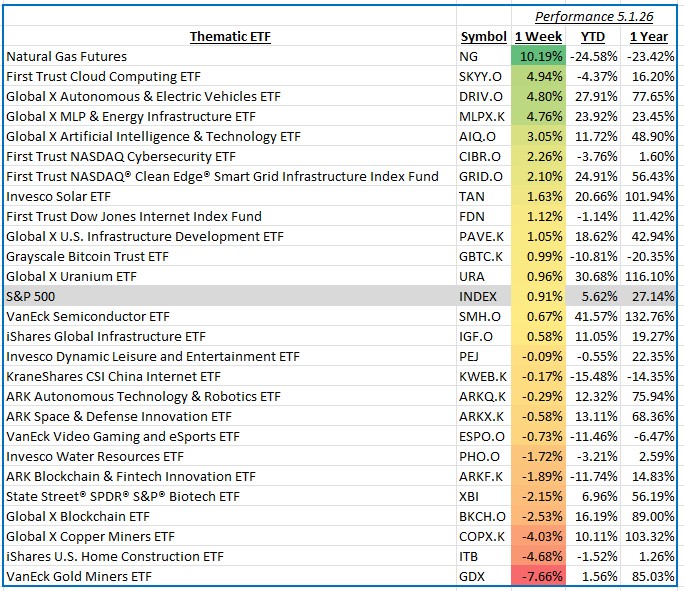

The S&P 500 advanced 0.91% for the week ending May 1, 2026, as investors continued to favor growth-oriented and thematic investment areas supported by strong earnings momentum and improving risk appetite. Within thematic equities, market leadership centered around artificial intelligence infrastructure, digital transformation, and energy-related investments. Investors also monitored interest rate expectations closely following mixed economic data, while commodity volatility and geopolitical developments continued to influence sector rotation across global markets.

Within the energy transition and commodity-linked investment themes, natural gas exposure delivered the strongest performance of the week, gaining 10.1% as cooler weather forecasts, tightening storage expectations, and rising global demand pushed prices sharply higher. Midstream operators, liquefied natural gas infrastructure companies, and exploration firms benefited from the move. Strong contributors included Cheniere Energy, Kinder Morgan, Williams Companies, and EQT Corporation, as investors responded positively to improving pricing dynamics and growing export demand tied to global energy security concerns.

Technology and digital infrastructure themes also performed well, led by cloud computing strategies that advanced 4.9% during the week. Continued enthusiasm surrounding artificial intelligence adoption, enterprise software spending, and expanding data center demand supported the group. Microsoft, Amazon, Alphabet, Snowflake, and ServiceNow were among the largest contributors as investors favored companies positioned to benefit from long-term growth in cloud services, cybersecurity, and AI-enabled productivity tools. Semiconductor and networking firms tied to hyperscale infrastructure spending also provided support across the broader technology ecosystem.

Precious metals and resource extraction themes experienced weakness, with gold miners declining 7.7% as easing safe-haven demand and a stronger U.S. dollar pressured gold prices. Investors rotated away from defensive commodity exposures as equity markets stabilized and Treasury yields moved modestly higher. Large mining operators including Newmont, Barrick Gold, Agnico Eagle Mines, and Franco-Nevada were among the primary detractors as declining bullion prices weighed on earnings expectations and investor sentiment across the group.

Housing and infrastructure-related themes also struggled during the week, with home construction exposure falling 4.7%. Higher mortgage rate concerns and persistent affordability challenges continued to pressure housing demand expectations despite relatively stable economic conditions. Major homebuilders including D.R. Horton, Lennar, PulteGroup, and Toll Brothers contributed to the decline as investors reassessed near-term earnings growth and order activity heading into the important spring selling season.

Overall, thematic equity markets reflected a continued preference for growth, technology infrastructure, and energy-related opportunities, while rate-sensitive and defensive areas faced pressure. Investors remain focused on earnings strength, monetary policy expectations, and evolving global growth trends as markets move further into the second quarter.