COMMENTARY:

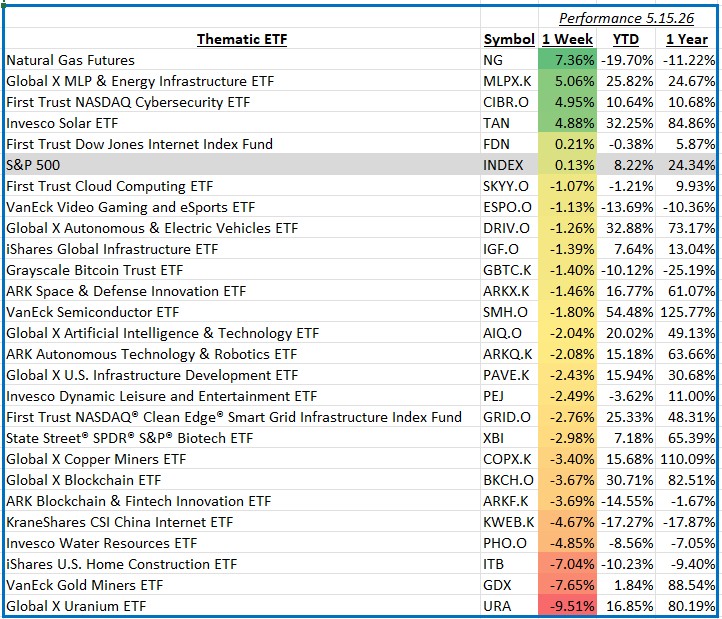

The S&P 500 returned a modest 0.13% for the week ending May 15, 2026, as powerful cross-currents in global commodity markets drove sharp divergences across thematic investment strategies. The near-total closure of the Strait of Hormuz continued to dominate headlines, sending energy prices sharply higher and reigniting inflation fears. Surging consumer and producer price data released during the week all but eliminated expectations for a Federal Reserve rate cut in 2026, with futures markets beginning to price in the possibility of a rate hike by year-end — a shift that rippled unevenly across growth, real assets, and infrastructure themes alike.

Energy — Natural Gas (Futures) (+7.4%) Natural gas was the top-performing commodity theme of the week, advancing 7.4% as the Hormuz closure disrupted global liquefied natural gas flows, tightening an already snug market. Iran’s South Pars field — the world’s largest natural gas reserve — remained partially offline, removing meaningful supply from international markets. Domestic U.S. production held near record levels, but surging LNG export demand from new Gulf Coast terminals, combined with growing electricity consumption from AI-driven data centers, continued drawing down inventories faster than expected.

Energy Infrastructure (+5.1%) Midstream energy infrastructure posted a strong 5.1% gain as pipeline and storage operators benefited directly from elevated throughput demand and higher commodity prices. Top holdings TC Energy, Enbridge, Williams Companies, Kinder Morgan, and ONEOK all contributed positively, as investors recognized the stable, fee-based cash flow model these companies offer — one that thrives regardless of whether oil prices are rising or simply remaining elevated. Rising inflation also reinforced the appeal of infrastructure as a real-asset hedge within diversified portfolios.

Uranium and Nuclear Energy — Laggard (−9.5%) Uranium miners were the week’s hardest-hit thematic group, falling 9.5% as rising Treasury yields and fading rate-cut hopes pressured growth-oriented, long-duration themes. Cameco, the largest holding and a dominant global producer, led the decline, while NexGen Energy, Oklo, and Uranium Energy also weighed heavily. The sector had run sharply higher on AI data center nuclear power demand, leaving valuations stretched and vulnerable to the hawkish macro repricing that defined the week.

Precious Metals Miners — Laggard (−7.7%) Gold miners fell 7.7%, an underperformance that reflected a sharp and counterintuitive dynamic: rising inflation weighed on gold rather than supporting it, as accelerating CPI and PPI data crushed rate-cut expectations and drove Treasury yields to their highest levels in nearly a year. Physical gold dropped roughly 4% for the week, pulling gold mining equities down with force. Newmont and Agnico Eagle, together the two largest holdings, led losses, with Barrick Mining, AngloGold Ashanti, and Wheaton Precious Metals also declining meaningfully as higher real rates eroded the appeal of non-yielding precious metal assets.

It was a week that rewarded tangible energy exposure and penalized rate-sensitive themes. With inflation running hotter than expected and geopolitical uncertainty showing no signs of abating, thematic investors are navigating a market that is simultaneously driven by commodity scarcity and monetary tightening — a challenging combination that is likely to keep volatility elevated in the weeks ahead.