Value has taken leadership from Growth in 2026, but the thematic ETF data suggest investors are repricing Growth rather than rejecting it. The market is moving away from broad, expensive Growth exposure and toward themes with clearer earnings visibility, cash-flow support or direct leverage to the AI capital-spending cycle.

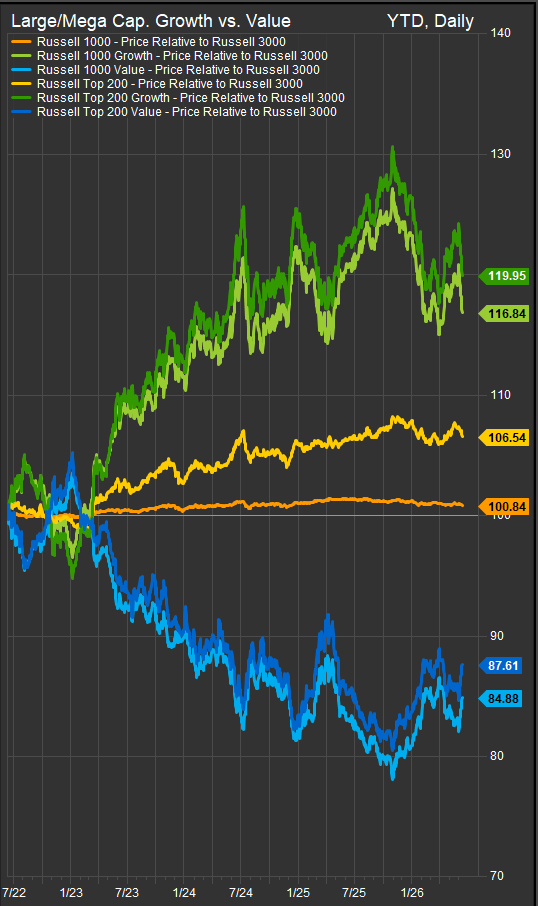

Chart: Russell large cap. style benchmarks relative to the S&P 500, 2022-present.

The broad style proxy confirms the shift. Vanguard Value ETF (VTV) outperformed Vanguard Growth ETF (VUG) across the latest week, month and six-month period. VTV gained 1.52% over the past week, 3.28% over the past month and 11.36% over six months. VUG declined 5.00% over the week, fell 1.95% over the month and gained 3.59% over six months. Flows also favored Value in the near term, with VTV attracting $814M over the past week and $2.15B over the past month, while VUG lost $215M over the week.

That does not mean the Growth bull market is over. It means Growth leadership is narrowing. Investors are still funding the AI buildout, but they are demanding more precision. The strongest thematic confirmation remains semiconductors, where ETFs attracted $4.37B over the past week, $7.22B over the past month and nearly $14.0B YTD. The category also gained 7.66% over the week and 74.1% over six months. SMH and SOXX remain the cleanest broad vehicles for the AI hardware cycle, with exposure to Nvidia, Broadcom, AMD, Taiwan Semiconductor, ASML and Marvell.

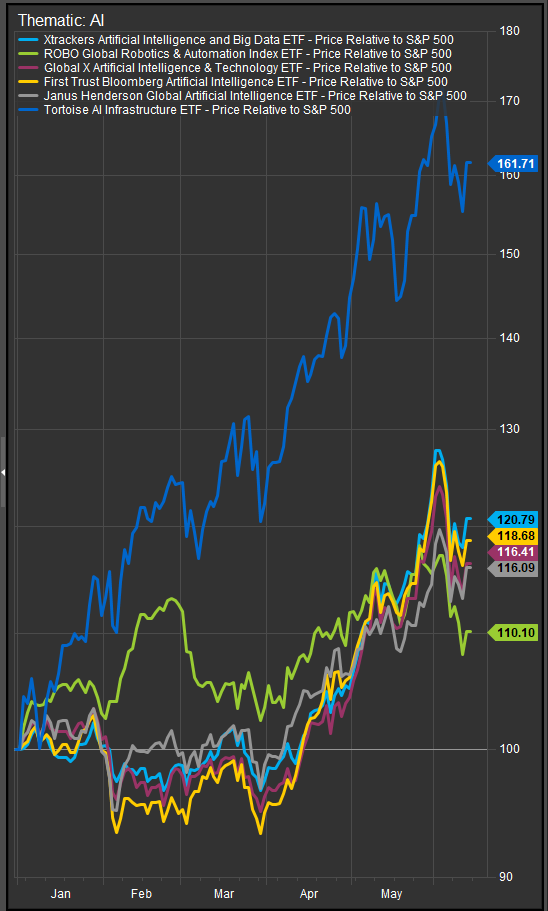

Chart: AI exposures still outperforming meaningfully in 2026.

The broader AI infrastructure trade also remains intact, but it is best viewed as a basket rather than a single-fund story. Investors continue to show interest in the assets required to scale AI: compute, memory, storage, data centers, networking, cooling, power equipment and grid infrastructure. Funds tied to semiconductors, electrification, infrastructure and robotics/AI capture different pieces of that value chain. TCAI remains one useful proxy inside that basket, but the larger point is that investors are still rewarding bottleneck exposure over speculative application-layer Growth.

The contrast with software is the key style message. Software ETFs still have $6.78B of YTD inflows and $1.53B of one-month inflows, but the category lost $850M over the past week and declined 3.29%. That short-term reversal reflects a more skeptical market view of AI monetization. Investors are asking whether freemium models, token-price competition, rising compute costs and heavy capex will dilute the margin opportunity for AI-enabled software platforms.

Thematic ETF Signals

| Theme / Proxy | 1W Flow | 1M Flow | YTD Flow | 1W Return | 6M Return |

| Semiconductors | $4.37B | $7.22B | $13.99B | 7.66% | 74.10% |

| Robotics & AI | -$0.10B | $0.82B | $6.16B | 2.41% | 24.86% |

| Software | -$0.85B | $1.53B | $6.78B | -3.29% | -1.25% |

| Disruptive Technology | $0.45B | $1.96B | $2.95B | 2.23% | 16.76% |

| Dividend | $0.65B | $5.31B | $42.91B | 0.42% | 8.88% |

| Finance/Fintech | $0.31B | $0.06B | -$0.91B | 1.61% | 3.68% |

| Natural Resources | -$1.65B | -$2.77B | -$8.30B | -1.88% | -0.02% |

Value’s thematic support is clearest in dividend and quality-income strategies. Dividend ETFs attracted $42.91B YTD, including $5.31B over the past month and $653M over the past week. SCHD remains the flagship example, with $11.13B of YTD inflows and 18.51% six-month performance. This is the market’s ballast trade: investors still want equity exposure, but they want more current cash flow and less dependence on multiple expansion.

Finance and fintech are also showing signs of improvement. The category attracted $306M over the past week and gained 1.61%, even though YTD flows remain negative. That fits the broader backdrop of stronger bank stocks, renewed IPO activity, private-credit demand and better capital-markets sentiment. In a style context, this is one of the ways Value is benefiting from higher nominal activity.

Natural resources are not confirming the inflation-hedge narrative. Despite geopolitical risk, energy volatility and metals-market stress, natural-resource ETFs lost $1.65B over the past week, $2.77B over the past month and $8.30B YTD. Investors are not yet treating inflation as a durable commodity-led regime shift. They are treating it as a risk to monitor rather than a reason to aggressively rotate into broad hard-asset exposure.

The Fed remains the pivot point. If inflation stays sticky and policy remains restrictive, Value, dividend, financials and select real-asset themes should continue to have an advantage. Higher discount rates make broad Growth harder to own, especially when earnings are distant or margins are uncertain. If inflation cools and the Fed becomes less restrictive, Growth should regain leadership, but likely through a narrower set of themes: semiconductors, AI infrastructure, high-quality platforms and automation rather than speculative software or unprofitable disruption.

Chart: Rising real yields have been a headwind to the broader Growth trade in 2026.

Chart: Risk appetite gages are firming based on our proxies and volatility gages have rolled over in the near term.

The conclusion is not that the Growth bull market is over. The easy phase of Growth leadership is over. From 2023 through 2025, investors rewarded broad AI exposure, mega-cap platforms and long-duration Growth. In 2026, the market is asking harder questions: who has earnings now, who benefits directly from AI capex, who has pricing power, and who can defend margins if AI services become cheaper?

The thematic ETF tape gives a clear answer. Growth still works when it is tied to infrastructure scarcity and earnings visibility. Value works when it is tied to cash flow, dividends and capital-market leverage. The weakest area is the middle: expensive Growth stories without clear margin durability and inflation hedges without confirming flows. For thematic investors, the current playbook favors semiconductor exposure, AI infrastructure baskets, dividend ballast and selective fintech, while remaining cautious on software until AI monetization becomes clearer.

Disclaimer: This material is for informational and educational purposes only and should not be considered investment advice, a recommendation to buy or sell any security, or a solicitation to engage in any investment strategy. ETF and benchmark performance figures are based on source data believed to be reliable but have not been independently verified. Past performance is not indicative of future results. Style investing, thematic ETFs and sector exposures may involve concentration risk, valuation risk, factor rotation risk, interest-rate sensitivity, geopolitical risk and sensitivity to changes in earnings expectations, inflation, Federal Reserve policy and investor sentiment. Investors should consult their own financial, tax and legal advisers before making investment decisions.