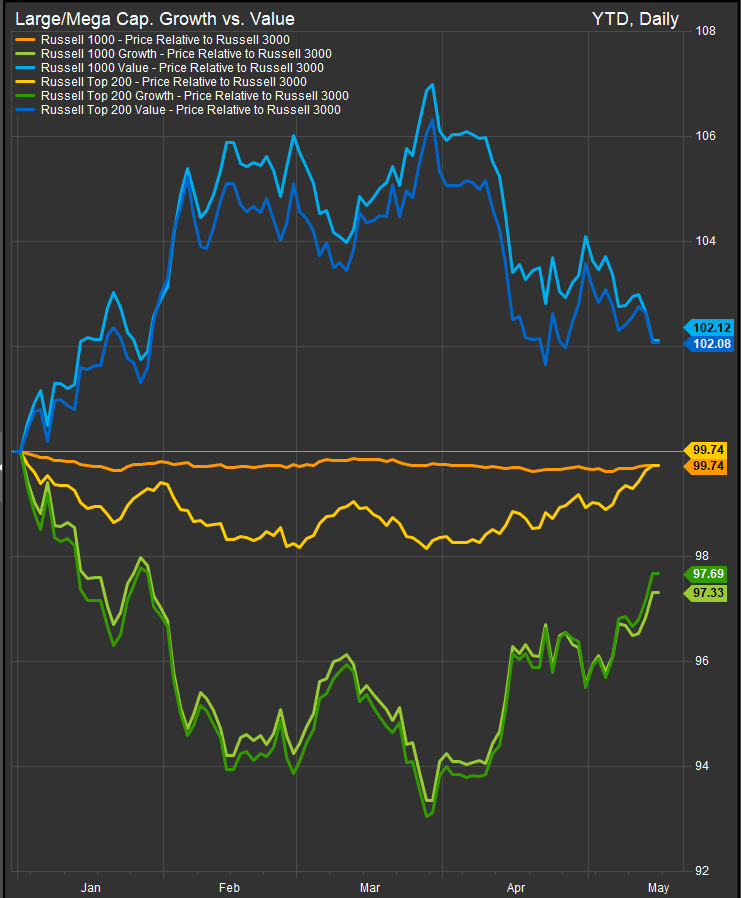

The Growth-versus-Value debate looks different through a thematic ETF lens. The factor scoreboard still favors Value: Russell 1000 Growth sits at 97.33, down 2.67% YTD relative to the Russell 3000, while Russell 1000 Value sits at 102.12, up 2.12% relative. Russell Top 200 Growth is down 2.31%, while Top 200 Value is up 2.08%.

But the thematic ETF tape is telling a more complicated story. Value has the YTD factor lead, yet investors are again paying for Growth-linked themes: semiconductors, robotics and AI, software, disruptive technology, momentum, and electrification. The result is not a clean Growth-versus-Value call. It is a barbell: investors want AI upside, but they also want dividend and cash-flow ballast.

That makes sense given the macro backdrop. The headlines are still Value-friendly: global yields are backing up, energy inflation is elevated, the Trump-Xi summit lacked major deliverables, and Middle East risk continues to pressure oil markets. BLS reported that April CPI energy prices rose 3.8% month over month, gasoline rose 5.4%, and core CPI rose 0.4%. BLS also reported April PPI final-demand services up 1.2% and final-demand goods up 2.0%. Reuters reported on May 15 that the 10-year Treasury yield rose to 4.54% and Brent crude approached $109, weighing on Nasdaq and S&P 500 futures.

In other words, the macro case still says Value should work. Higher yields and higher oil prices usually reward companies with nearer-term cash flows, cheaper valuations, dividend support, and more tangible earnings. That helps explain why Value is still ahead in the factor data.

Our thematic ETF database gives us a useful way to translate the Growth-versus-Value factor discussion into investable categories. On the Growth side, semiconductor ETFs such as SMH, SOXX, XSD, and PSI show how AI infrastructure has become the highest-beta expression of the Growth rebound. SMH was up 27.95% over one month and 68.16% over six months, while SOXX was up 32.10% over one month and 84.09% over six months. But the flows were more nuanced: SMH had $3.13B of YTD inflows but $2.02B of one-month outflows, suggesting some profit-taking after the surge.

For broader AI exposure, ETF’s BAI, AIQ, BOTZ, ARKQ, and ROBO offer exposure. These funds help show that AI is not just a mega-cap tech trade. BAI was up 22.80% over one month and had $3.12B of YTD inflows, while AIQ was up 20.45% over one month with $744M of YTD inflows. That supports the idea that investors are still allocating to AI implementation themes, not just passively riding Nasdaq exposure.

Software and cloud themes have also shown some resilience. IGV, SKYY, CIBR, HACK, BUG, and CLOU can be used to show where Growth is broadening beyond semiconductors. IGV had $5.68B of YTD inflows, even though its six-month return was still negative, while CIBR, BUG, and CLOU posted strong one-month gains. That helps make the point that investors are selectively buying beaten-down software, cybersecurity, and cloud names as AI monetization becomes more tangible.

The Momentum category is another clean bridge between factors and themes. SPMO, MTUM, XMMO, and PDP are useful examples. SPMO was up 16.48% over one month and had $2.09B of YTD inflows, while MTUM was up 13.66% over one month with $1.11B of YTD inflows. That supports the argument that the Growth rebound is not only thematic; it is also showing up in factor momentum.

On the Value side, the strongest examples are not necessarily traditional Value ETFs alone, but dividend, energy, infrastructure, and real-asset exposures. SCHD, VIG, VYM, DGRO, and CGDV are useful dividend examples. SCHD had $8.20B of YTD inflows and was up 18.91% over six months, while CGDV had $4.79B of YTD inflows and a 6.54% one-month return. That fits the article’s barbell conclusion: investors want Growth upside, but they are still putting large amounts of capital into income and cash-flow strategies.

For energy and commodity-linked Value exposure, XOP, OIH, FCG, AMLP, MLPX, KOPX, GLD, and SLV. OIH was up 56.28% over six months, XOP was up 27.71%, and KOPX was up 49.54% with $2.30B of YTD inflows. But GLD and SLV had meaningful YTD outflows despite positive six-month returns, which shows that resource exposure is not a uniform flow winner.

For infrastructure and electrification, inflows have accrued to PAVE, IFRA, GRID, VOLT, POWR, ICLN, and QCLN. GRID stands out with $3.85B of YTD inflows, an 8.87% one-month return, and a 29.59% six-month return. That gives the Growth side of the article an important nuance: electrification and power infrastructure are both AI-adjacent and real-asset-adjacent, sitting between Growth and Value rather than cleanly belonging to either style.

The conclusion from the returns is clear: Growth-linked themes are leading tactically, while Value remains the more durable macro hedge. If yields keep rising and oil inflation persists, Value, dividends, energy, infrastructure, and cash-flow themes should remain relevant. If yields stabilize and AI monetization broadens, semiconductors, AI, software, momentum, and electrification can keep leading.

For thematic ETF investors, the better question is not “Growth or Value?” It is which Growth, and which Value? The Growth side is AI infrastructure, semiconductors, software, robotics, and momentum. The Value side is dividend income, legacy energy, infrastructure, and selected real-asset exposure. The data argues for a barbell: participate in the AI-led rebound, but do not ignore the rate-and-inflation regime that put Value ahead in the first place.

Sources

- FactSet Research Systems Inc.

- StreetAccount (News flow)

- LSEG / FTSE Russell — Russell U.S. Style Indexes and Growth/Value framework.

- LSEG / FTSE Russell — Russell style methodology using book-to-price, forecast growth, and sales-per-share growth.

- BLS — April 2026 Consumer Price Index summary.

- BLS — April 2026 Producer Price Index summary.

- Reuters — May 15, 2026 market reaction to inflation, yields, oil, and risk-off pressure.

- Reuters — Big Tech debt issuance to fund AI and cloud expansion.

- Reuters — Applied Materials guidance and AI-driven semiconductor equipment demand.

- Reuters — Figma revenue outlook and AI monetization.

Disclaimer: This material is for informational and educational purposes only and is not investment advice, a recommendation, or an offer to buy or sell any ETF, security, strategy, or investment product. Past performance does not guarantee future results. ETF flows and returns can change quickly.