March 2, 2026

We will be delivering bi-monthly reviews of our Kaleidoscope Thematic Model to help investor track reactions to the changing macro picture through actual allocation decisions in the financial markets. Our model is a core strategy that skews aggressive given the high overlap of Growth themes with the most popular thematic investment categories. Later this month we will be debuting our companion model, currently under development, which is an income and low vol. exposure.

The past month saw economic data soften and investors shift towards low vol equities, government credit and precious metals. Natural resources exposures continued to benefit while Mega Cap. Growth stocks remained under pressure.

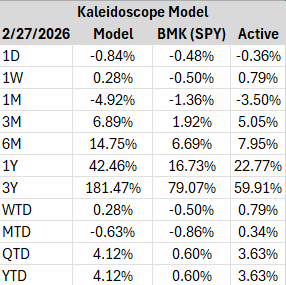

The past month was less about earnings noise and more about structural repricing. The Kaleidoscope Thematic Equity Model declined -4.92% versus -1.36% for SPY, resulting in -3.50% active underperformance. The drivers were not random — they reflected a clear rotation in how markets are pricing liquidity, geopolitical risk, and growth duration.

The model’s architecture across Commodities, Industrial, Technology, and Consumer pillars makes these rotations visible in real time.

Table: Model Rolling Performance Through 2/27/2026

Liquidity Regime Shift: Pressure on Digital Duration

The dominant structural story over the past month has been the repricing of long-duration growth and liquidity-sensitive assets.

The Technology sleeve — particularly digital asset and innovation-linked exposures — drove the bulk of the decline:

- GBTC -1.05%

- BKCH -0.96%

- SMH -0.54%

- SKYY -0.50%

- KWEB -0.62%

- ARKF -0.57%

This is not idiosyncratic weakness. It reflects a broader structural shift in market tone. As macro uncertainty rises and financial conditions tighten, markets compress duration risk. Innovation beta, crypto-linked assets, and high-multiple software are typically the first areas to reprice.

The Kaleidoscope Model intentionally holds structural exposure to these areas because they represent long-term secular change — digital scarcity, AI infrastructure, decentralized finance. In short-term tightening regimes, however, they will exhibit elevated volatility.

This month was a clear reminder of that dynamic.

Hard Assets Reassert Themselves

While innovation beta compressed, hard asset exposure showed resilience.

Within the Commodities sleeve:

- NANR +0.52%

- COPX +0.30%

- GDX +0.33%

The positive performance of gold and copper miners during a month of broader equity weakness underscores an important structural theme: markets are still pricing geopolitical fragmentation, capital scarcity, and resource discipline.

Copper reflects electrification and industrial demand. Gold reflects monetary uncertainty and geopolitical stress. The fact that these exposures held firm while growth beta sold off reinforces the diversification logic embedded in the model’s four-pillar structure.

Hard assets are not tactical trades here — they are structural counterweights to duration risk.

Infrastructure and Industrial Capacity: The Middle Ground

The Industrial sleeve remained constructive:

- GRID +0.30%

- PAVE +0.31%

- IGF +0.29%

These exposures represent the physical implementation of structural policy: grid modernization, infrastructure buildout, energy transition investment. Their stability suggests that capital expenditure cycles remain intact even as capital markets reprice risk.

In a world of reshoring, infrastructure spending, and energy system redesign, industrial capacity remains a durable structural theme. The relative resilience of these ETFs during a volatile month supports that narrative.

Consumer Themes: Cyclical Sensitivity Emerging

The Consumer sleeve was mixed:

- ITB +0.19%

- ESPO -0.20%

- DRIV -0.02%

Homebuilders’ resilience suggests that domestic balance sheets remain stronger than feared. However, discretionary digital leisure and EV-adjacent themes softened alongside broader risk sentiment.

Structurally, this reflects a consumer that is stable but selective — resilient in housing and essentials, more cautious in speculative or growth-adjacent spending.

Structural Takeaways

The trailing month illustrates three structural realities:

- Duration sensitivity remains the market’s primary fault line.

Technology and digital asset exposures are highly responsive to liquidity expectations. When policy uncertainty rises or rates drift higher, these sleeves will amplify downside volatility. - Real assets and capital-cycle themes remain relevant.

Commodities and infrastructure exposures continue to provide balance in an environment defined by geopolitical stress and capital discipline. - Diversification across independent structural drivers matters.

The Kaleidoscope Model’s passive, quarterly-rebalanced framework does not attempt to forecast regime shifts. Instead, it maintains exposure across structural pillars so that leadership rotation is captured over time.

The Bigger Picture

The Kaleidoscope Thematic Equity Model is designed to express structural transformation, not short-term momentum. Over longer horizons — 3 months (+6.89%), 1 year (+42.46%), and 3 years (+181.47%) — the diversified thematic structure has demonstrated its ability to compound when secular forces align.

The past month reflects the cost of maintaining exposure to innovation beta during liquidity compression. But it also reinforces why the model includes commodities and industrial capacity alongside technology and consumer evolution.

Structural change does not move in straight lines.

Liquidity cycles shift.

Geopolitics reprice risk.

Innovation continues.

The Kaleidoscope framework is built to navigate all of it — not by predicting the next headline, but by allocating across the forces that shape them.

Model Constituent Rolling Performance and Current Portfolio Weights: 2/27/2026

Data sourced from FactSet Research Systems

Attribution is for commentary only and should not be construed as investible research or investment advice. Models do not take into account trading costs and attribution is not GIPS compliant.